Best Way to Buy a House in Canada

While in that location are many reasons why owning a habitation is a desirable outcome, it is a big commitment and you demand to make sure that you are fully prepared for all that it entails. It requires stability, responsibility and financial discipline. Renting might feel like y'all are falling behind while paying somebody else'due south mortgage, merely it does afford you a high degree of flexibility and much less responsibility. If you are notwithstanding at a phase in your life where yous are experiencing uncertainty in aspirations, career or relationships, you may want to expect a chip before you lot decide to purchase a home. Home-ownership is a great long-term investment, simply if yous end up selling inside the get-go couple of years of the initial purchase, it is probable that transaction costs (Realtor, Lawyer, etc...) would exceed what you would accept otherwise paid in hire. Potentially college future interest rates can also bear on the affordability and return on investment of buying a business firm. If the but reason y'all are considering home-ownership is to participate in an affectionate housing market, call back there are plenty of other means to invest in real manor without owning property yourself. Existent estate investment trusts (REITs), existent estate commutation traded funds (ETFs), mutual funds, and publicly traded real manor focused companies such equally commercial developers, hotel chains, and real estate management firms are all viable ways to invest in real estate without owning property. Rent vs. Buy Estimator When buying a house, yous need a articulate picture of what and where you lot would like to buy in order to avoid settling for a sub-optimal outcome. Having a well-defined, realistic property objective helps y'all evaluate all potential outcomes against your expectations and determine whether or not to go on. In this stage y'all'll desire to give a lot of thought to how your belongings objective fits into your broader plans for life and any potential problems that could arise. Make sure to consider how owning a abode in a item location may affect your career, family, mobility, recreation, and retirement goals going frontwards. You lot will also want to be enlightened of the costs associated with different types of backdrop - for example condo fees, maintenance, utilities, insurance, and the differences in property taxes in diverse urban and rural areas. Don't crusade yourself a hidden cost headache downward the road. Understand that different property types and locations have unlike rules, regulations, and financing requirements that likewise may affect the feasibility of your goals. PRO TIP: Talk with a mortgage broker early in the process. A broker is familiar with many unlike lenders and their lending rules and tin can assist you determine what property objectives are realistic and within your financial attain. One of the first questions any prospective home-buyer should exist asking is "are my home-ownership goals financially feasible?" In other words, can you get a mortgage? To lend hundreds of thousands of dollars to you lot, lenders demand to ensure that you are financially capable of reliably managing all of your existing financial obligations in addition to your new mortgage and other home-ownership related costs, even in the face of an unforeseen setback such as unemployment. To appraise your financial worthiness, lenders consider three different wide indicators of financial health in context with the property type, value, and location that you are considering. Although property specific conditions and regulations may vary, lenders are legally obligated to consider your Income, your Credit, and the Equity (down payment) y'all accept available earlier they decide to lend you any money. You tin use the handy acronym I.C.Due east to remember this. A mortgage professional can help you navigate these requirements. To qualify for a mortgage in Canada, you lot have to exist able to prove that you lot reliably earn plenty income to cover all of your debts and expenses. This includes all existing debts and expenses such equally vehicle loans, credit cards, lines of credit, and educatee loan payments, as well as your new mortgage, belongings taxes, and an allowance for expected abode heating costs. What you can beget with the income at your disposal is determined by a maximum ratio of monthly debt payments and expenses to monthly income. When it comes to affordability, at that place are two ratios that lenders consider. The Gross Debt Service Ratio (GDSR) is the percentage of your gross (pre-revenue enhancement) income that is required to pay for housing related costs including the mortgage, property taxes, utilities, and 50% of whatever condo fees. To authorize for a mortgage, it is recommended that your GDSR does not exceed approximately 35% to 39%. At that place are some exceptions for situations in which the down payment exceeds 20% of the purchase toll. The Total Debt Service Ratio (TDSR) is the percentage of your gross (pre-tax) income that is required to cover all housing related costs considered in the GDSR plus all of your other debts such as credit cards, vehicle payments, lines of credit, alimony and child support, etc. Except for cases involving large downwards payments (>xx%) your TDSR tin can not exceed 44%. Income requirements vary depending on your employment blazon (self-employed, probation, guaranteed vs non-guaranteed hours, or contract piece of work) as well as the size of your down payment. RULE OF THUMB: More often than not, the mortgage/house you tin get canonical for will be nether 4.5x your gross taxable almanac household income. Mortgage Calculators (what can you beget?) Earlier they approve you lot for a mortgage, mortgage lenders desire to see that you have a reliable runway record of paying your debts and bills. To do this, lenders will assess your credit history by looking at your credit report. A credit study is a recorded history of how y'all come across your fiscal obligations over fourth dimension. It records the types of credit you have had, the balances you've carried, your payment history, likewise as whatever past involvement with collections, consumer proposals, or bankruptcy. Your credit data is so mathematically translated into a 3-digit numerical credit score (FICO score) between 300 and 900 using a points and weighting system. Many lenders are looking for a credit score of at least 650 to approve you for a mortgage. It is recommended that you obtain a copy of your credit report early on in your habitation-buying process so as to avoid any unfortunate surprises further downwardly the line. Poor or insufficient credit is a mutual claiming faced by many prospective home-buyers. Luckily, credit can be fixed or established with some subject, only information technology does take time, so better to kickoff sooner rather than afterward. The best ways to keep your credit report looking shiny is to: Different lenders have dissimilar credit requirements, so if one says no, that doesn't mean they all will. A mortgage banker tin can assist you amend sympathize your credit besides as the different lending options available to yous in your particular situation. Finally, yous must have some of your own money "on the table" to get a mortgage in today'due south lending environment. This is called your down payment, and - although there are ways to synthesize a cypher-downwardly mortgage in special situations - the rule is y'all need to have your own disinterestedness stake (ie. your savings) to get a mortgage. There are diverse adequate sources of down payment. A downwardly payment is defined as the corporeality of the property's buy price that you supply yourself at the time of purchase (ie. your downwardly payment/equity + mortgage loan = holding purchase price). The minimum downward payment required to become a mortgage depends on: Generally, for a good credit, tax-paying Canadian looking to purchase an owner-occupied home in an urban area, the minimum required down payment is: Acreages crave larger downward payments and raw land / vacant lot purchases generally require much larger down payments. If you have under twenty% downwardly payment, yous volition too need mortgage default insurance, which is automatically added to the mortgage balance and payment. This type of insurance protects the mortgage lender from loss in the upshot that you lot neglect to make your mortgage payments. Information technology does not protect you. For people with infrequent credit and low debt-to-income ratios who simply practise non have the required savings to purchase a home, it is possible to borrow some or all of the minimum 5% down payment on a separate line of credit, or personal loan. Information technology is also possible for a family unit member to gift some or all of the downward payment every bit long as this is properly documented. If y'all are buying your get-go home, in that location are certain programs available to you to help make your first purchase a fiddling easier. If y'all recall that you come across the income, credit, and equity requirements to purchase a home in Canada, so the side by side step is to get pre-canonical for a mortgage. This will assistance you lot make up one's mind what yous can afford and identify any unforeseen obstacles that y'all volition take to bargain with. Delight understand the difference betwixt a pre-qualification discussion and the much more than rigorous pre-blessing process. A pre-qualification is substantially a general statement on what mortgage amount y'all could likely get based on your stated income and debt load. It assumes you have the required down payment for the property-type you are subsequently and there is no real review of your documents or credit report. Sound confusing? Well it is - there are many variables to lending, and the devil is in the details that can only exist uncovered in a more thorough review that is an bodily pre-blessing. Information technology is recommended that you get pre-qualified very early on in the procedure so that you have an idea of any potential issues, qualifying amounts, and to help frame your planning. For example, why dream near a $400,000 home when your income and debt load tin only support a much smaller amount? We call this a " Discovery Telephone call ." A pre-approval is a comprehensive review of a mortgage application, credit report, and all documents that will be used to support your mortgage objective, followed by a written statement confirming that yous run into the income, credit, and down payment requirements for a loan of a sure value for a specific property type. In that location are typically a number of weather condition fastened and the pre-blessing is only temporarily valid. You should become pre-approved for a mortgage before y'all begin shopping for a property as that process volition confirm y'all can indeed be approved when the time comes and removes dangerous assumptions near your income, credit or down payment from the process. Sellers and realtors will as well accept you more than seriously. It's of import to notation that pre-approval is not a guarantee of a final approval as the holding you lot cull still must encounter the conditions of your lender, and so ever make your offering of purchase provisional on financing. Although some banks may advertise quick and easy pre-qualification or approval processes, go on in mind this is only for the lending options that they provide and will not provide a full picture of the entire mortgage lending market. They also have limited options to aid you if y'all practice not run into their strict requirements.Click hither to read about the full mortgage approval procedure. Working with a mortgage banker gives you admission to a much broader range of mortgage financing options than working with an individual lending institution. Banks and other mortgage lenders make their mortgage products available to mortgage brokers and compete for your business. Brokers are able to shop among them on your behalf to obtain lending solutions and great deals based on the specifics of your needs and circumstances. While y'all might be able to authorize for a mortgage at your usual depository financial institution, it is important to understand that the representatives in that location are acting in the interests of their employer and accept no incentives to advise the mortgage products of other lenders that may have more suitable options. Brokers are able to act as intermediaries between you lot and the various potential lenders in guild to present a range of potential mortgage options. A mortgage broker does non cost you annihilation because they get paid a commission by the mortgage lender (not you lot) just when they successfully fund your mortgage. The end effect is a great rate, more pick and better communication. If you are unsure whether you lot meet the requirements for a mortgage, click the get started button to provide the states with some initial information and we will allow you know if an opportunity exists. Tabular array of Contents There are many lenders in Canada and even more than lending programs, merely not all volition apply or be right for you. A mortgage is a loan for a real estate property, but it is not a i size fits all financial product and there are a number of variables to consider. In addition to the size of the mortgage that you lot cull/qualify for, yous will also need to consider the mortgage rate, amortization menses, term, payment frequency, and any potential penalties you could incur downwardly the route. At that place are as well add-ons and special offers to think about depending on your financial situation and what you are trying to attain. The mortgage charge per unit is the interest charge per unit that you are expected to pay back to the lender in addition to the initial principal that you borrow. Think of it as the rental rate for coin. The mortgage rates bachelor to you depend on a variety of factors including your financial state of affairs, the holding type, the contract term, and external economic factors that touch all interest rates. Rates can either bestock-still (locked in for the term of your mortgage) or variable (floating rate that is subject area to changing economic conditions). The lowest rate does not ever mean the lowest toll for your mortgage equally at that place are other considerations such as penalties, portability, and restrictions on your ability to qualify. The acquittal catamenia is the amount of fourth dimension it will take yous to fully pay off your mortgage by post-obit a pre-determined payment schedule. The longest amortization period currently permitted in Canada for mortgages with nether twenty% down payment is 25 years. The acquittal period is broken down into periods of time known as terms during which the contractual parameters of the mortgage have legal effect. After each term the remaining mortgage residual must exist renewed (recalculated at current rates with either the same or a more competitive lender), refinanced (renegotiated with additional funds borrowed), or paid for in full (usually not an option). Y'all keep renewing your mortgage until your firm is fully paid off. The most pop term (with the nigh competitive rates) is v years, but it can be as trivial as half-dozen months or equally much equally ten years. Yous will also need to select a payment frequency. This is but how often y'all brand payments against the balance of your mortgage. Many people will cull to sync up their payment schedule with their paychecks. The more frequently that you make payments, the less you cease up spending in interest over the life of your mortgage. This is because you pay off more of the balance in between each time the mortgage is compounded (when interest is calculated and added to the total balance). If y'all take less than 20% downward payment, y'all will demand mortgage default insurance from a provider such as CMHC or Genworth. This protects lenders (not you) in the event that you cannot or do not make your payments and default on your loan. Mortgage loan insurance is calculated as a pct of your total loan amount and is typically higher for smaller down payments. It tin usually exist paid up front or added to your mortgage loan. Dissimilar lenders and lending programs take dissimilar penalties included in their contracts that you should exist aware of, which can be incurred for numerous reasons such as terminating your mortgage before the end of your mortgage term (this is often the case if you sell the property). Finally, there are add together-ons and special offers such every bit purchase plus improvements programs (packet the cost of planned renovations into your mortgage), beginning time home-buyer assistance programs, and limited time rate offers. A mortgage broker makes choosing the right mortgage easier because, unlike bank reps, they have admission to a much wider range of lending products and are not tied to one line of business. This allows them to make recommendations that are more specific to your personal situation and negotiate on your behalf between lenders to obtain ameliorate terms and conditions than would otherwise exist available. Once you have mortgage pre-approval in hand, you can brainstorm to search for a holding that fits with your financial capabilities. Keep in mind that just considering you have been pre-approved for loan of a certain value does not hateful you should spend that much on a house. Choosing a holding that costs less than the maximum you could afford leaves you lot a little wiggle room in the event of unexpected changes in interest rates, your expenses, or your ability to earn money. When searching for a house, information technology is important to consider not only your current needs, but also how those needs may evolve over the side by side 5 or x years. Consider how a potential belongings fits into your ongoing career, family, and lifestyle goals. A clear picture of your needs and goals helps y'all avoid settling for a property that might cause you frustration downwards the route. To determine how well a particular property fits your housing needs, there are 5 property specific considerations. Be sure to take the fourth dimension to do your research and don't allow yourself to rush or feel pressured into any hasty decisions. The choices you make today will impact your lifestyle and finances for years to come. Having the correct Realtor on your side can help y'all appraise your options and ensure you get a property that is right for you. Similar a mortgage banker, a Realtor can be an invaluable source of information and guidance during the abode-buying process. Realtors should be an expert in the communities in which they operate and in their local real estate markets. Not only can they aid observe the right property for you, just they can as well help you negotiate the best deal and navigate regional and situational complexities using their local knowledge. Real estate markets become up and down all the time. Realtors take admission to by and comparable sales data and empathise the market history and trends which can aid you identify a good fourth dimension to buy and determine how much you should be willing to pay. Realtors are also helpful when information technology comes to submitting offers and managing paperwork, contracts, and title transfer complexities. In addition to keeping track of everything and ensuring you don't miss something important, they as well aid yous to salvage a considerable amount of time over the grade of the home-buying process. When it comes to choosing a Realtor, trust is key. Y'all need to make sure that the person representing you through ane of the biggest decisions of your life is somebody who you tin can rely on to provide dependable communication and expertise. Ask for recommendations from friends and relatives or look at listings in the areas yous are considering to identify industry leaders. Feel free to conduct interviews to find i that you feel comfy working with. Realtors tend to specialize in different areas of the existent estate market, and so it is important to know where and what yous are looking for before you brainstorm working with ane. Understand that Realtors are held answerable by a code of conduct that ensures that they represent y'all to the fullest of their abilities without conflict of interest and insures you against negligence or incompetence on the part of the amanuensis. To avert conflict of involvement, nosotros suggest y'all avoid calling the Realtor whose name is on the listing yous are interested in if yous are looking for someone to represent you. Ask yourself, how tin can that person correspond both your best interests (get you the lowest toll for instance) and the seller'due south all-time interest (get them the highest toll)? You will likely need to sign an Agency Service Agreement which gives the Realtor the right to correspond yous for a certain menses of time. Some agreements are improve than others so go to know your Realtor a flake and make sure you lot trust and can work with them before yous agree to sign anything. Remember that like mortgage brokers, most Realtors are paid a commission but when the bargain is finalized, and so employ their time and services only if you intend to follow-through with a buy (ie. be loyal to those that aid y'all). One time you have found a property that meets your requirements and is within your price range, it is time to make an offer. Your Realtor's task is to help you make an offering. Using past comparable sales data and their knowledge of market trends they can help yous identify good value for your coin and make up one's mind what you should be willing to offer. This allows y'all to move quickly on well-priced properties that meet your criteria. Even with professional representation, it is nonetheless of import to do your own research too. You should have a broad view of what similar properties are listed for and - more importantly - insight into what like backdrop are actually selling for. While it can exist emotional, it's best to be armed with facts and knowledge to make the decision more rational and mechanical. And call up, if one door closes (deal not quite right), another door will open up! If you lot are working with a Realtor, they volition handle the specifics of submitting an offer to purchase, but information technology is still a good idea to have a basic idea of what an offer looks similar. An offer to purchase, if accepted, is a legally binding contract between the buyer and the seller that establishes the parameters of the transaction. It includes the legal names of the parties involved in the transaction, a description of the property, included unattached goods (chattels) such as appliances or furniture, excluded fastened appurtenances (fixtures), financial details of the transaction, all conditions, stipulations and deadlines, and the closing date; whereupon you get the keys. Don't exist afraid to negotiate. While it tin can exist uncomfortable for some, this is a big purchase and it is all about finding the optimal middle ground betwixt you and the seller. The seller may exist manner more motivated to sell than you are to buy their particular holding vs. others on the marketplace. That could mean a peachy bargain for you if yous have washed your homework on pricing. When you are gear up to submit an offer of purchase, it is important that y'all include a condition of finance (COF) deadline which indicates a engagement past which you will accept your mortgage financing secured and finalized. This is a deadline that you get to choose. If you make the deadline also fast and are unable to arrange your financing in time, you could lose the deal if some other buyer comes along. Bold that you have already been pre-approved for a mortgage (full review of income, credit and downwardly payment including document review), you can set a slightly tighter financing deadline, merely remember that the specific property that you choose still must run into the atmospheric condition of your specific lender to finalize your mortgage approval. An unrealistic deadline puts a lot of force per unit area on you and the system in full general, peculiarly during decorated times. Generally, we recommend that you lot (via your Realtor) set the Condition of Finance or COF date to x business days afterwards the seller has accustomed the offering, rather than choosing a specific date. That way if negotiations drag on, the COF is non inadvertently compressed. For an insured mortgage on an urban firm with Realtors involved and your pre-approval in hand, financing tin ordinarily be arranged within 5-7 business organisation days. Where a concrete appraisement is required (non-insured mortgage) vii+ business days, and for remote properties with outbuildings, potential condition issues, or for individual transactions let for at least 10-fourteen business organization days. More than time is always meliorate for you, then don't let yourself be pressured into a brusk borderline! Too keep in mind that the lenders with the everyman interest rates are the busiest, so they too demand more time. You lot may also want to make your offer subject area to boosted conditions such every bit a home inspection or satisfactory review of condo documents (if buying a condo). These conditions also must exist satisfied within the specified time frame. When your offering is accustomed by the seller, you will need to make an firsthand deposit of funds to secure the property. This is "skilful faith money" to verify your buying intent and will be credited toward your downward payment when you buy. Never give your deposit directly to the seller. Instead, the eolith check should be made out "in trust" to the seller's real manor agent's brokerage office or to a lawyer until all weather condition of the offer to purchase accept been satisfied. If one or more of the purchase weather condition are not satisfied, then the money is returned to you. Yet, if the conditions are all satisfied and accepted and then you lot cannot complete the deal for whatever reason, you will likely lose your deposit. A deposit of 1-2% of the purchase price is typically enough, but sometimes more is required. Once the bargain is finalized, the deposit is credited as part of the down payment. Information technology is condign increasingly common for home-buyers to make their offering to purchase provisional on home inspection. Sellers don't have a motivation to disclose whatsoever potential problems or concerns with the condition, safe, structure, or functionality of the property and not all defects are easily apparent. The purpose of a home inspection is to uncover any potential defects in the holding, its systems, its components, and the surrounding land before getting locked into a contract to purchase. Information technology is of paramount importance that the habitation inspector you choose is trustworthy, experienced, and reliable. Practise your research on how to choose a home inspector and find one with a reputable rails record and specific abode inspection experience and grooming. The goal is to be completely confident that there are no unexpected issues with electrical, plumbing, heating, roofing, foundation, structure, interior and outside. Avoid price shopping as cutting costs on a home inspector could cost you thousands if they miss something. The skillful ones might cost a picayune more! If you are buying a condo, you should also make your offer bailiwick to a satisfactory review of the condo documents. You will want to obtain copies of the condominium reserve fund study, its fiscal statements, and the latest annual general meeting minutes from the condo board. What you are looking for is any indication of poor financial management on the role of the governing body of the condo corporation and whatever mention of a "special assessment" (a levy imposed past the condo lath on condo owners in excess of their normal condo fees to account for an unexpected shortfall in the budget). Ask your Realtor if they tin recommend a Condominium Document Review specialist if you are not sure what you are looking for. In one case the seller has accepted your offer and weather condition, your mortgage professional volition work with y'all to finalize your mortgage approval prior to your Condition of Financing deadline. Provided that your mortgage pre-approval was conducted competently and the property y'all have chosen meets all of the lender's requirements, there shouldn't be any surprises at this stage. (Meanwhile, you and your Realtor volition exist working on the other purchase conditions, such as the property inspection). Your mortgage professional will require a re-create of the accepted Offer to Purchase and an MLS Listing Sheet containing the property details, which your Realtor can provide. Your electronic application is updated with the property details and financing borderline. Your mortgage banker will review their list of preferred lenders and place a target lender with the best rate and terms for your situation. Your property details and loan application are then submitted to that lender via Filogix Express™ and queued electronically. Normal queue time for underwriting is 24-48 hours. Sometimes during the busy jump season, there is a longer expect time in the queue (48-72+ hours) before an underwriter reviews your application (this can slow an approval). For a mortgage broker, a fast lender queue is definitely a factor in choosing who to submit to, just sometimes available rates and terms justify the wait (the best lenders are typically the busiest!). Mortgage underwriting is the process a lender uses to determine if the risk of lending to a particular borrower nether certain parameters is acceptable. Retrieve of an application like a chair with 4 legs which correspond your income, credit, downwardly payment, and the holding itself. In order for your awarding to successfully support a loan all 4 legs should exist proportional and stable. If one leg is a bit weaker than the others, the application all the same might stand, but with multiple weak legs, the application collapses. A thorough pre-approval should prevent any surprises at this stage and will decide which lenders are suitable to submit to. If a lender declines to provide a mortgage delivery or is taking too long and you are working with a mortgage broker, they can re-submit for approval to the next best lender. If your application meets the lender's underwriting guidelines, your mortgage professional person will produce an electronic "commitment" signifying that your application has been approved subject field to a listing of lending conditions that you would yet demand to satisfy. The weather condition volition stipulate what documents are required to prove income, avails, employment, property details and value (for example, an acceptable appraisal, discussed below). If the loan terms are acceptable to you, y'all accept their offer (sign the commitment) and fix virtually to meet the applicable lending conditions. Generally, the majority of the loan conditions volition be satisfied by documents that you take already collected and are sitting in your mortgage professional person's file if indeed y'all were properly pre-canonical for a mortgage (awarding, credit review and document review). You may demand to update your file with a more contempo pay stub, or an update on your downwardly payment savings if the file copies are too one-time. Having washed a pre-approval with document review in advance really speeds up the procedure and avoids nasty surprises, therefore yous should make certain this step happens early on on. There is unremarkably a certificate review queue at the lender's finish, so the faster you tin can get the accepted commitment and 100% of the required support documents to the lender, the faster you tin can get to "file complete," whereby all "broker" conditions take been met and accepted by the lender. The lender then triggers "mortgage instructions" to be sent to your selected lawyer. At this indicate, your mortgage professional will propose you, your Realtor (if applicable) and your lawyer, in writing that funding has been "canonical." If there is a financing condition on an Offer to Purchase, your Realtor can now lift that status. As mentioned above, before any mortgage is finalized, your mortgage lender will crave a property valuation or appraisement in some class. This is to ensure that the coin they are lending you, plus your downwards payment, practise not exceed the fair market place value for the belongings as adamant by a licensed appraiser. Appraisals are conducted past licensed appraisers who determine what the property is worth based on comparable sales data for the surface area. This is different from a Realtor's comparative market analysis and is also not the same thing as a dwelling house inspection. Typically, lenders volition require that the appraisal is conducted by an appraiser that is on their specific "canonical list" and volition accept instructions on what can be included and what cannot in the valuation of the property. For example, most residential lenders volition not attribute any value to outbuildings such as barns, shops, and sheds. An appraiser may or may not physically visit the property, as in that location are electronic methods too; it depends on the lending situation. Site visits will certainly be required for private purchase transactions, refinances, mortgages that volition not be CMHC-insured, acreages, foreclosures, any MLS listing where property status issues are noted, and oft when the purchase price is reduced after the offer was accepted/habitation inspection. Your mortgage professional will order and coordinate the appraisal. After the condition of financing and any other contractual stipulations have been met and conditions lifted, the deal is "ready to close" and the mortgage professional, your Realtor, the mortgage lender and your lawyer begin to coordinate the last phase of your purchase transaction, called Conveyancing and Funding. Congratulations on getting this far. Yous have near bought your first habitation! Pour yourself a beverage of your choice and celebrate the milestone! The work isn't over yet however, as in that location is nonetheless lots to practise before you are comfortably moved in. Y'all will need to suit utilities contracts, get property insurance, do some cyberbanking and encounter with the lawyer. Coming up, you will - in most cases - be coming together with your lawyer or notary to conclude or "close" your transaction. Here'due south what to expect next: There is often confusion around what to practice about utilities when moving. Before y'all motility you will desire to contact your current service providers for power, gas, cable, telephone and net and inquire as to whether they operate in the area you lot are moving to. If they exercise you will probable be able to transfer whatsoever existing contracts to your new residence. Otherwise you lot will accept to abolish existing contracts (hopefully without paying a penalty) and arrange new ones to be in place for when you move into your new home. Brand certain that when you lot cancel or update your contracts that you record the date, time and name of the person y'all talked to. It can happen that something gets inputted into a arrangement wrong and y'all want to be able to show that it was not your fault and that yous did everything correct. A forgotten or improperly canceled contract could show upward as a negative on your credit report, not to mention exist a hurting to correct. These days, many provinces allow you lot to purchase natural gas and power from independent "free energy retailers" and information technology can be confusing. First you need to effigy out which pipeline or electrical company services the area (ask the town or city function), then what are the free energy supply options. My full general advice is merely enquire for the "default / regulated supply option." Here is a web log I wrote on the topic. Property insurance Equally part of the weather condition of funding, your mortgage lender volition require you to have property/fire insurance, which is to protect y'all (and the lender) confronting financial loss from amercement to your property due to an unforeseen event such as a fire or overflowing. Imagine losing your house to a fire while still owing a significant portion of your mortgage loan - that could be catastrophic! Start with the insurance company where y'all have your tenant or vehicle insurance and go from there. Your lawyer will be asking you to bring in an "insurance binder letter" to the upcoming pre-closing meeting. Life and disability insurance While you are not obligated to accept life and/or inability insurance, it'southward strongly recommended that you lot review your needs at this point in time. These protect you and your family from losing the home in the event there is a loss of income (death or disability) and notwithstanding a mortgage to pay. There are 2 types of life and inability insurance to consider.Mortgage life insurance is easy to become and the payout is tied to your mortgage residual which diminishes every bit you pay information technology off. Term life insurance is an independent life insurance policy which may have more requirements to qualify for, but the payout is independent of your remaining mortgage rest. Sometimes it'due south easiest to sign up for mortgage life insurance at the fourth dimension of mortgage approval then abolish it if or when you are able to find a amend term life policy. Insurance Brokers are similar mortgage brokers; they can store the market for you. Banks often accept their ain insurance divisions. Here is a link to read more on life insurance. Note: CMHC mortgage default insurance has goose egg to practise with the items higher up. If you are nonetheless dislocated, ask your mortgage professional or lawyer and they will be able to explain any questions that you might have. Depending on where in Canada you lot are buying, you may need to pay a land transfer tax as part of your endmost costs. This can be a big boosted expense. Revenue enhancement rates vary from province to province and in some cases from municipality to municipality. Neither Alberta nor Saskatchewan have state transfer taxes. Some provinces such every bit Ontario and British Columbia offer beginning-fourth dimension-buyer land transfer tax exemptions to assist make it easier to purchase your beginning habitation. Ask your Realtor nigh this taxation when you lot first see. Tabular array of Contents There are several things you can do to brand moving into your new habitation easier. Starting early on and keeping organized rather than leaving everything to the last minute is probably the number one thing that you can do to brand your move easier. Brand a listing of everything that you will need to accomplish and organize it into dissimilar time horizons. Congratulations on buying your first abode (and for making it to the bottom of this ridiculously long page). We promise this guide has been of value to you. If we missed anything or there is annihilation else you'd like to know, please let united states of america know and we volition be happy to address it for you lot. If yous would like to have u.s.a. on your home-ownership team, we would be happy to prepare y'all up with a free consultation to discuss the specifics of your situation. Make up one's mind if Home-Ownership is Right for Yous

Decide Where and What to Buy

Understand the Fiscal Requirements to Buy a House

Income

Credit

Equity / Down Payment

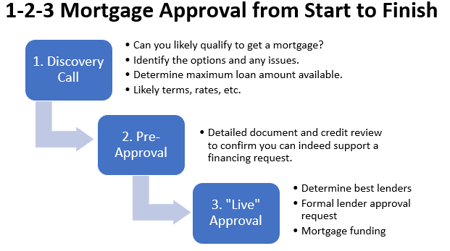

Get Pre-Canonical for a Mortgage

How Mortgage Brokers Help

Choosing the Right Mortgage

Search for Potential Houses

How Realtors Aid

How to Choose a Realtor

Make an Offer to Purchase

Components of an offering to purchase

Condition of Financing

Deposits

Property Inspection

Review Condo Documents

Finalize Your Mortgage Approval

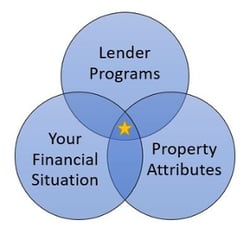

Lender Underwriting (takes 1 - 7 days from a formal submission)

Conditional Commitment Processing (takes 2 - 4 days from lender approval)

Property Valuation

Shut the Deal

What to Look with the Lawyer

Utilities

Insurance

Land Transfer Taxes and Title Transfer Fees

Moving Checklist

One month before your movement

Two weeks before your move

One week before your motion

A few days before your move

Motility solar day!

After your move

Enjoy Your Home

How to Buy a Business firm ( Summarized)

More Resources

Buying a Residential Property in Canada

First Fourth dimension Homebuying Process - steps for preapproval, and so steps to buy

Free Guide - Homebuying Stride by Pace

Gratuitous Guide - Newcomers to Canada

Costless Guide - Condominium Heir-apparent's Guide

CMHC Housing Outlook - what are the experts saying well-nigh housing prices

Blog for Home Buyers - Richards Mortgage Group - subscribe, larn, stay in-impact

Using Your RRSP for Down Payment - larn the rules

Financing Your Home Purchase

Mortgage Broker vs Banking company - who will help y'all more?

Tin You Get a Mortgage? - learn what it takes to quailfy

Setup a Pre-Approval Meeting - gear up to get started?

Mortgage Rates - rate isn't everything, merely information technology is important.

Mortgage Approval Procedure

Free Guide - 3 Steps to Successful Mortgage Shopping

Mortgage Calculators - fix for some math (or telephone call usa!)

Apply Now - start a mortgage application

Rent-to-Ain for Buyers - another way to finance, when banks say no

Rent-to-Own for Sellers - some other way to sell your home

Vendor Financing - other fashion to finance, when banks say no

Heir-apparent Assistance Programs

Souvenir Letter Template - your family can help with down payment

Qualifying for a Mortgage - what lenders await at

Mortgage Default Insurance - what is information technology?

Mortgage FAQs

Re-Financing Your Home

Free Guide -Renewing & Renegotiating Your Mortgage

Free Guide -Borrowing On Home Disinterestedness

Gratuitous Guide -Pay Off Your Mortgage Faster

Renew vs Refinance - what's the deviation?

Gratuitous 15 infinitesimal Renewal Consultation

Contrary Mortgages - seniors tin tap into home disinterestedness without moving or making payments

Financing Home Improvements

Understanding Credit

Free Guide - Agreement Your Credit Score

Credit Score Comeback Program

Secured Credit Cards

Mortgages in Full general

Mortgage Rates

Calculators

Glossary

Mortgage FAQs

For Nerds!

Insurance

Mortgage Default Insurance

Mortgage Life Insurance

Life Insurnace Check-up

Property / Fire Insurance

Disability Insurance

Piece of work Disruption

Title Insurance

Source: https://www.richardsmortgagegroup.ca/how-to-buy-a-house-canada

0 Response to "Best Way to Buy a House in Canada"

Post a Comment